diff --git a/README.md b/README.md

index 6afa775c..43f47bdc 100644

--- a/README.md

+++ b/README.md

@@ -10,34 +10,25 @@

**QuantStats** Python library that performs portfolio profiling, allowing quants and portfolio managers to understand their performance better by providing them with in-depth analytics and risk metrics.

-[Changelog »](./CHANGELOG.md)

-### QuantStats is comprised of 3 main modules:

-

-1. `quantstats.stats` - for calculating various performance metrics, like Sharpe ratio, Win rate, Volatility, etc.

-2. `quantstats.plots` - for visualizing performance, drawdowns, rolling statistics, monthly returns, etc.

-3. `quantstats.reports` - for generating metrics reports, batch plotting, and creating tear sheets that can be saved as an HTML file.

-

----

-

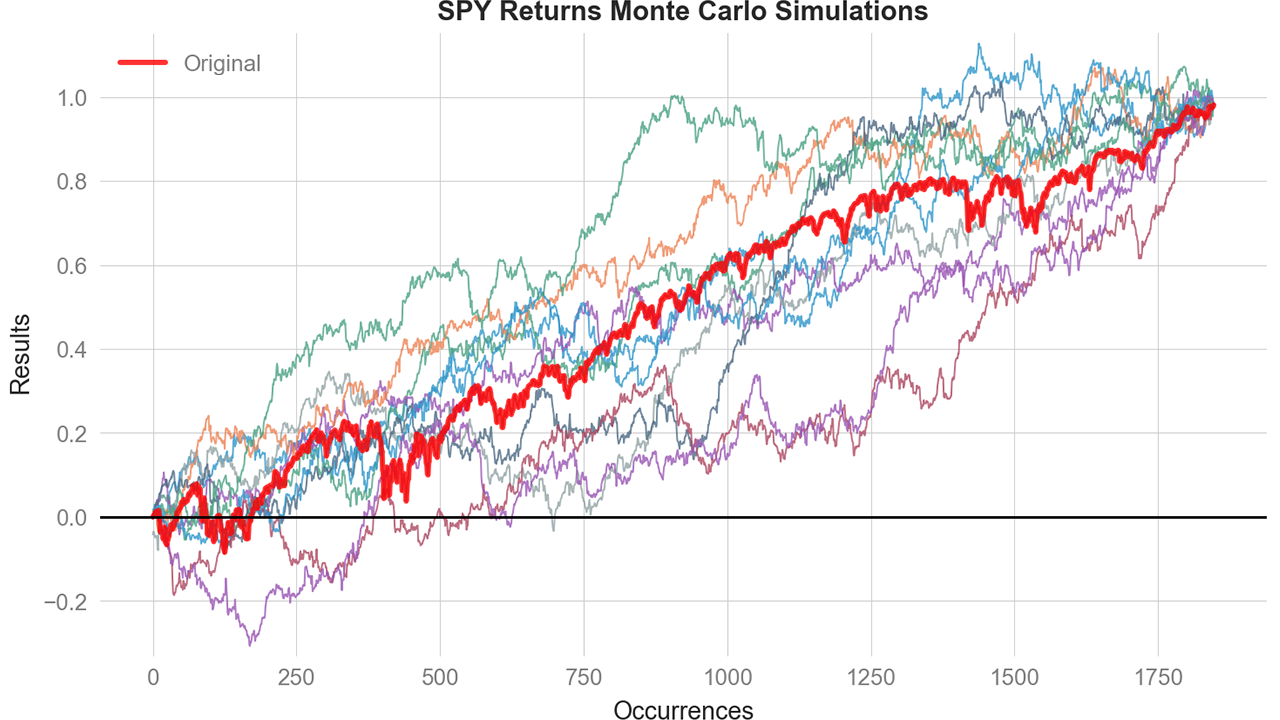

-### **NEW! Monte Carlo Simulations**

-

- -Run probabilistic risk analysis with built-in Monte Carlo simulations:

+## Navigation

+- [Quick Start](#quick-start)

+- [Understanding Returns](#understanding-returns-important)

+- [Documentation](docs/docs_and_api_ref.md)

+ - [NEW! Monte Carlo Simulations](docs/montecarlo.md)

+- [Installation](#installation)

+- [Questions and Contributions](#questions-and-contributions)

+- [Changelog »](./CHANGELOG.md)

-```python

-mc = qs.stats.montecarlo(returns, sims=1000, bust=-0.20, goal=0.50)

-print(f"Bust probability: {mc.bust_probability:.1%}")

-print(f"Goal probability: {mc.goal_probability:.1%}")

-mc.plot()

-```

-[Full Monte Carlo documentation »](./docs/montecarlo.md)

+## Quick Start

----

+### QuantStats is comprised of 3 main modules:

-## Quick Start

+1. `quantstats.stats` - for calculating various performance metrics, like Sharpe ratio, Win rate, Volatility, etc.

+2. `quantstats.plots` - for visualizing performance, drawdowns, rolling statistics, monthly returns, etc.

+3. `quantstats.reports` - for generating metrics reports, batch plotting, and creating tear sheets that can be saved as an HTML file.

```python

%matplotlib inline

@@ -47,13 +38,13 @@ import quantstats as qs

qs.extend_pandas()

# fetch the daily returns for a stock

-stock = qs.utils.download_returns('META')

+returns = qs.utils.download_returns('META')

# show sharpe ratio

-qs.stats.sharpe(stock)

+qs.stats.sharpe(returns)

# or using extend_pandas() :)

-stock.sharpe()

+returns.sharpe()

```

Output:

@@ -71,9 +62,15 @@ qs.plots.snapshot(stock, title='Facebook Performance', show=True)

# stock.plot_snapshot(title='Facebook Performance', show=True)

```

-Output:

+Output (full-size version [here](https://github.com/ranaroussi/quantstats/blob/main/docs/snapshot.webp?raw=true)):

-

+

-Run probabilistic risk analysis with built-in Monte Carlo simulations:

+## Navigation

+- [Quick Start](#quick-start)

+- [Understanding Returns](#understanding-returns-important)

+- [Documentation](docs/docs_and_api_ref.md)

+ - [NEW! Monte Carlo Simulations](docs/montecarlo.md)

+- [Installation](#installation)

+- [Questions and Contributions](#questions-and-contributions)

+- [Changelog »](./CHANGELOG.md)

-```python

-mc = qs.stats.montecarlo(returns, sims=1000, bust=-0.20, goal=0.50)

-print(f"Bust probability: {mc.bust_probability:.1%}")

-print(f"Goal probability: {mc.goal_probability:.1%}")

-mc.plot()

-```

-[Full Monte Carlo documentation »](./docs/montecarlo.md)

+## Quick Start

----

+### QuantStats is comprised of 3 main modules:

-## Quick Start

+1. `quantstats.stats` - for calculating various performance metrics, like Sharpe ratio, Win rate, Volatility, etc.

+2. `quantstats.plots` - for visualizing performance, drawdowns, rolling statistics, monthly returns, etc.

+3. `quantstats.reports` - for generating metrics reports, batch plotting, and creating tear sheets that can be saved as an HTML file.

```python

%matplotlib inline

@@ -47,13 +38,13 @@ import quantstats as qs

qs.extend_pandas()

# fetch the daily returns for a stock

-stock = qs.utils.download_returns('META')

+returns = qs.utils.download_returns('META')

# show sharpe ratio

-qs.stats.sharpe(stock)

+qs.stats.sharpe(returns)

# or using extend_pandas() :)

-stock.sharpe()

+returns.sharpe()

```

Output:

@@ -71,9 +62,15 @@ qs.plots.snapshot(stock, title='Facebook Performance', show=True)

# stock.plot_snapshot(title='Facebook Performance', show=True)

```

-Output:

+Output (full-size version [here](https://github.com/ranaroussi/quantstats/blob/main/docs/snapshot.webp?raw=true)):

-

+

+  +

+

### Creating a report

@@ -92,113 +89,39 @@ Let's create an html tearsheet:

qs.reports.html(stock, "SPY")

```

-Output will generate something like this:

-

-

-

-[View original html file](https://rawcdn.githack.com/ranaroussi/quantstats/main/docs/tearsheet.html)

-

-### Available methods

+Output (full-size version [here](https://rawcdn.githack.com/ranaroussi/quantstats/main/docs/tearsheet.html)):

-To view a complete list of available methods, run:

+

+  +

+

+### The Returns object

+As seen in previous examples, QuantStat's primary input is a time-series:

```python

-[f for f in dir(qs.stats) if f[0] != '_']

+returns = qs.utils.download_returns('META')

+qs.stats.sharpe(returns)

```

-

+Or a dataframe (several series with a shared index):

```python

-['avg_loss',

- 'avg_return',

- 'avg_win',

- 'best',

- 'cagr',

- 'calmar',

- 'common_sense_ratio',

- 'comp',

- 'compare',

- 'compsum',

- 'conditional_value_at_risk',

- 'consecutive_losses',

- 'consecutive_wins',

- 'cpc_index',

- 'cvar',

- 'drawdown_details',

- 'expected_return',

- 'expected_shortfall',

- 'exposure',

- 'gain_to_pain_ratio',

- 'geometric_mean',

- 'ghpr',

- 'greeks',

- 'implied_volatility',

- 'information_ratio',

- 'kelly_criterion',

- 'kurtosis',

- 'max_drawdown',

- 'monthly_returns',

- 'montecarlo',

- 'montecarlo_cagr',

- 'montecarlo_drawdown',

- 'montecarlo_sharpe',

- 'outlier_loss_ratio',

- 'outlier_win_ratio',

- 'outliers',

- 'payoff_ratio',

- 'profit_factor',

- 'profit_ratio',

- 'r2',

- 'r_squared',

- 'rar',

- 'recovery_factor',

- 'remove_outliers',

- 'risk_of_ruin',

- 'risk_return_ratio',

- 'rolling_greeks',

- 'ror',

- 'sharpe',

- 'skew',

- 'sortino',

- 'adjusted_sortino',

- 'tail_ratio',

- 'to_drawdown_series',

- 'ulcer_index',

- 'ulcer_performance_index',

- 'upi',

- 'value_at_risk',

- 'var',

- 'volatility',

- 'win_loss_ratio',

- 'win_rate',

- 'worst']

+returns = DataFrame()

+returns["META"] = qs.utils.download_returns('META')

+returns["TSLA"] = qs.utils.download_returns('TSLA')

+qs.stats.sharpe(returns)

```

-```python

-[f for f in dir(qs.plots) if f[0] != '_']

-```

+Quantstats makes several notable assumptions about this object by default:

+1. This is a daily (`datetime64[s]` index) time-series of returns (`float64`). These returns are the percent gain from the previous period (e.g. 10% growth -> 0.1, NOT 1.1).

+2. There are 252 periods (rows) in a year (not 365!) corresponding to the number of trading days in the U.S. stock market. Many methods assume this amount of periods by default; if you have substantially more or less data in your time-series, the annualization math may be skewed.

+3. For an example of correctly shaped returns, see time-series returned by `qs.utils.download_returns()`

-```python

-['daily_returns',

- 'distribution',

- 'drawdown',

- 'drawdowns_periods',

- 'earnings',

- 'histogram',

- 'log_returns',

- 'monthly_heatmap',

- 'montecarlo',

- 'montecarlo_distribution',

- 'returns',

- 'rolling_beta',

- 'rolling_sharpe',

- 'rolling_sortino',

- 'rolling_volatility',

- 'snapshot',

- 'yearly_returns']

-```

-**\*\*\* Full documentation coming soon \*\*\***

+## Additional Notes

-### Important: Period-Based vs Trade-Based Metrics

+### Period-Based vs Trade-Based Metrics

QuantStats analyzes **return series** (daily, weekly, monthly returns), not discrete trade data. This means:

@@ -216,17 +139,9 @@ For **discretionary traders** with multi-day trades, these period-based metrics

This is consistent with how all return-based analytics work (Sharpe ratio, Sortino ratio, drawdown analysis, etc.) - they operate on return periods, not discrete trade entries/exits.

----

-

-In the meantime, you can get insights as to optional parameters for each method, by using Python's `help` method:

-

-```python

-help(qs.stats.conditional_value_at_risk)

-```

+### Help on function conditional_value_at_risk in module quantstats.stats:

```

-Help on function conditional_value_at_risk in module quantstats.stats:

-

conditional_value_at_risk(returns, sigma=1, confidence=0.99)

calculates the conditional daily value-at-risk (aka expected shortfall)

quantifies the amount of tail risk an investment

@@ -246,7 +161,7 @@ Install using `conda`:

$ conda install -c ranaroussi quantstats

```

-## Requirements

+### Requirements

* [Python](https://www.python.org) >= 3.10

* [pandas](https://github.com/pydata/pandas) >= 1.5.0

@@ -258,7 +173,7 @@ $ conda install -c ranaroussi quantstats

* [yfinance](https://github.com/ranaroussi/yfinance) >= 0.2.40

* [plotly](https://plot.ly/) >= 5.0.0 (optional, for using `plots.to_plotly()`)

-## Questions?

+## Questions and Contributions

This is a new library... If you find a bug, please

[open an issue](https://github.com/ranaroussi/quantstats/issues).

@@ -266,11 +181,6 @@ This is a new library... If you find a bug, please

If you'd like to contribute, a great place to look is the

[issues marked with help-wanted](https://github.com/ranaroussi/quantstats/issues?q=is%3Aopen+is%3Aissue+label%3A%22help+wanted%22).

-## Known Issues

-

-For some reason, I couldn't find a way to tell seaborn not to return the

-monthly returns heatmap when instructed to save - so even if you save the plot (by passing `savefig={...}`) it will still show the plot.

-

## Legal Stuff

**QuantStats** is distributed under the **Apache Software License**. See the [LICENSE.txt](./LICENSE.txt) file in the release for details.

diff --git a/docs/docs_and_api_ref.md b/docs/docs_and_api_ref.md

new file mode 100644

index 00000000..e40f0641

--- /dev/null

+++ b/docs/docs_and_api_ref.md

@@ -0,0 +1,143 @@

+## Further References

+

+

+Full documentation is still in the works. In the meantime...

+

+1. Many methods already contain detailed docstrings in the source code, so refer to those for further information on each method's parameters, return values, and additional information.

+

+2. AI-Generated Documentation can be found [here](https://deepwiki.com/ranaroussi/quantstats/1-overview).

+

+3. You can get insights as to optional parameters for each method, by using Python's `help` method:

+

+```python

+help(qs.stats.conditional_value_at_risk)

+```

+

+## API Reference

+

+```python

+import quantstats as qs

+

+qs.extend_pandas()

+

+df.cagr()

+qs.cagr(df)

+```

+

+### Stats

+

+Many of the methods below in qs.stats can be extended onto Pandas' Time-series and DataFrame objects. For more information, refer to qs.extend_pandas()

+

+```python

+[f for f in dir(qs.stats) if f[0] != '_']

+```

+

+```python

+['avg_loss',

+ 'avg_return',

+ 'avg_win',

+ 'best',

+ 'cagr',

+ 'calmar',

+ 'common_sense_ratio',

+ 'comp',

+ 'compare',

+ 'compsum',

+ 'conditional_value_at_risk',

+ 'consecutive_losses',

+ 'consecutive_wins',

+ 'cpc_index',

+ 'cvar',

+ 'drawdown_details',

+ 'expected_return',

+ 'expected_shortfall',

+ 'exposure',

+ 'gain_to_pain_ratio',

+ 'geometric_mean',

+ 'ghpr',

+ 'greeks',

+ 'implied_volatility',

+ 'information_ratio',

+ 'kelly_criterion',

+ 'kurtosis',

+ 'max_drawdown',

+ 'monthly_returns',

+ 'montecarlo',

+ 'montecarlo_cagr',

+ 'montecarlo_drawdown',

+ 'montecarlo_sharpe',

+ 'outlier_loss_ratio',

+ 'outlier_win_ratio',

+ 'outliers',

+ 'payoff_ratio',

+ 'profit_factor',

+ 'profit_ratio',

+ 'r2',

+ 'r_squared',

+ 'rar',

+ 'recovery_factor',

+ 'remove_outliers',

+ 'risk_of_ruin',

+ 'risk_return_ratio',

+ 'rolling_greeks',

+ 'ror',

+ 'sharpe',

+ 'skew',

+ 'sortino',

+ 'adjusted_sortino',

+ 'tail_ratio',

+ 'to_drawdown_series',

+ 'ulcer_index',

+ 'ulcer_performance_index',

+ 'upi',

+ 'value_at_risk',

+ 'var',

+ 'volatility',

+ 'win_loss_ratio',

+ 'win_rate',

+ 'worst']

+```

+

+### Plots

+

+```python

+[f for f in dir(qs.plots) if f[0] != '_']

+```

+

+```python

+['daily_returns',

+ 'distribution',

+ 'drawdown',

+ 'drawdowns_periods',

+ 'earnings',

+ 'histogram',

+ 'log_returns',

+ 'monthly_heatmap',

+ 'montecarlo',

+ 'montecarlo_distribution',

+ 'returns',

+ 'rolling_beta',

+ 'rolling_sharpe',

+ 'rolling_sortino',

+ 'rolling_volatility',

+ 'snapshot',

+ 'yearly_returns']

+```

+

+### Reports

+

+```python

+[f for f in dir(qs.reports) if f[0] != '_']

+```

+

+```python

+['Path',

+ 'StringIO',

+ 'basic',

+ 'full', 'html',

+ 'metrics',

+ 'plots',

+ 'relativedelta',

+ 'tempfile',

+ 'webbrowser']

+```

\ No newline at end of file